J. Risk Financial Manag. 2024, 17(5), 206; https://doi.org/10.3390/jrfm17050206 (registering DOI) - 14 May 2024

Abstract

This study examines stock market response (SMR) to the Japanese tourism industry (TI) after the government’s announcement of travel subsidies (TRSs) during the COVID-19 pandemic in 2020, using a sample comprising 80 listed Japanese firms in the TI and an event study method

[...] Read more.

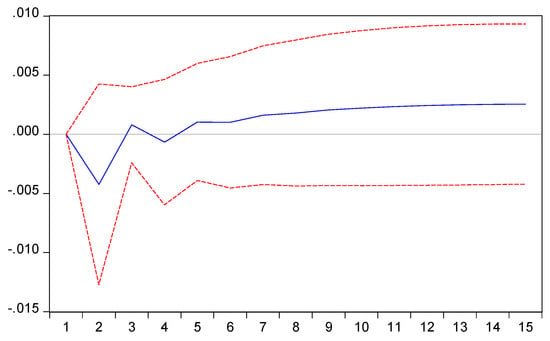

This study examines stock market response (SMR) to the Japanese tourism industry (TI) after the government’s announcement of travel subsidies (TRSs) during the COVID-19 pandemic in 2020, using a sample comprising 80 listed Japanese firms in the TI and an event study method (ESM) to determine the impact of government policy responses (GPRs) to the pandemic. This study found that investors in the TI reacted positively to the announcement of subsidies; this positive effect persisted for 50 trading days after the announcement but was weaker for transportation firms. The results suggest that TRSs are important for the TI, with a stronger link to travel-related firms, such as airlines and travel agencies, hotels, and amusement services. However, investors in the TI reacted negatively to policies that directly addressed the pandemic, such as social distance policies (SDPs). These results are robustly confirmed when we measure abnormal returns by using a three-factor model. The results offer useful insights for policymakers and practitioners aiming to mitigate economic loss from disasters such as the COVID-19 pandemic.

Full article

(This article belongs to the Special Issue Financial Markets and Institutions)

►

Show Figures

Figure 1

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}